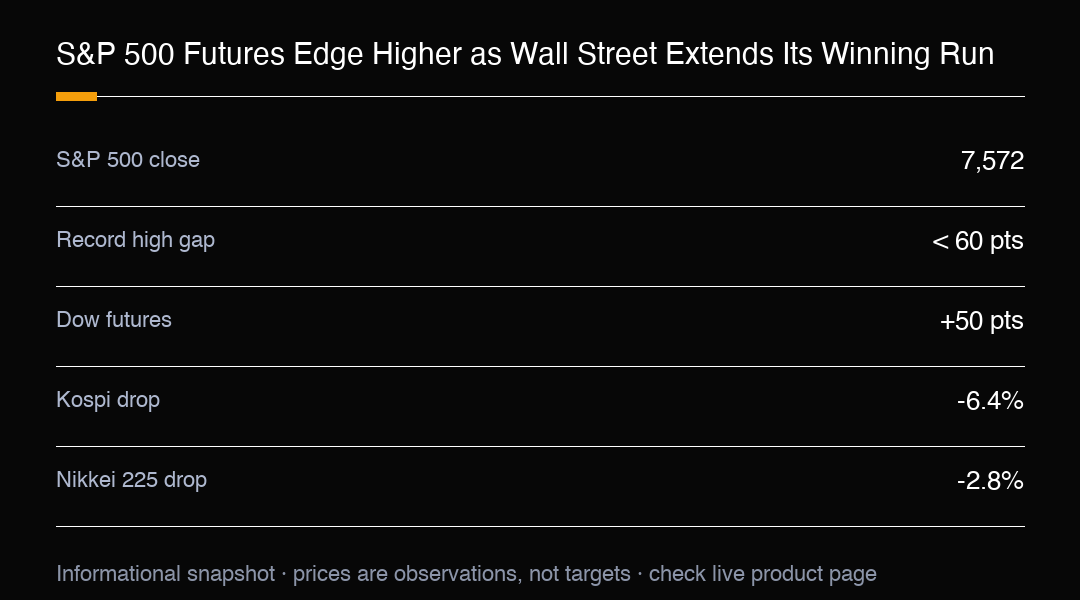

US equity futures nudged higher on Thursday after another winning session on Wall Street, with the S&P 500 pushing closer to a fresh all-time high. Dow futures added about 50 points, while S&P 500 and Nasdaq 100 futures each gained around 0.1%, a sign that traders were prepared for more upside heading into the open.

The S&P 500 finished the prior session at 7,572, leaving it fewer than 60 points beneath its record peak. The familiar market question lingers: when does the run pause, if at all? For now, momentum is doing the talking, and the index keeps grinding higher on the back of megacap strength rather than broad participation.

Apple, Alphabet and Amazon each climbed more than 3% in the latest session, more than offsetting weakness in chipmakers. It was not a flawless rally, but the heavyweight names proved more than capable of carrying the broader market uphill on their own, a pattern that has defined the advance for weeks.

A softer producer price index helped the mood. The PPI, which tracks the prices businesses pay before goods reach consumers, came in below expectations and reinforced hopes that inflation is cooling. Lower Treasury yields added to the support, since bond yields and stock valuations often move in opposite directions; when yields fall, fast-growing companies, especially in technology, tend to look more attractive.

Strong earnings from major banks strengthened the view that corporate America is still delivering healthy profits even as price pressures ease. The combination of softer inflation data and resilient profits is the backdrop bulls have been waiting for, and it has kept dip-buyers active on every small pullback.

Attention now turns to retail sales, jobless claims and a slate of high-profile company results for the next batch of market-moving cues. Each release will be read through the same lens: does it confirm that growth is slowing gently rather than breaking, which would let the soft-landing narrative stay intact?

While Wall Street kept smiling, Asia had a rougher morning. South Korea's Kospi slid roughly 6.4%, briefly triggering a trading halt after heavyweight chipmakers SK Hynix and Samsung Electronics dropped 11% and 8% respectively. The weakness spilled over from US semiconductor shares after SK Hynix ADRs fell about 9% overnight alongside names such as Micron and Intel.

Japan's Nikkei 225 lost 2.8%, and policy headlines did little to steady sentiment. South Korea delivered its first rate hike since 2023, while Japan again signalled it could step in to support the yen. Traders largely shrugged at both developments, keeping the focus on the tech-led divergence between regions rather than on central-bank signalling.

The split between a calm US tape and a volatile Asian session is a useful reminder of how uneven this rally has become. US indices are led by a handful of mega-cap winners, while export-facing Asian markets are wrestling with currency pressure and a cooling semiconductor cycle at the same time.

For traders weighing the next move, the setup is clear: US indices remain in a strong uptrend supported by cooling inflation and solid earnings, but the sharp Asia sell-off shows risk can rotate quickly across markets. Watching yield direction and mega-cap leadership will be key to judging whether the S&P 500 finally closes the gap to its record high or stalls just short of it.

Beneath the index level, market breadth tells a more cautious story. With so much of the gain concentrated in a few megacap names, a broadening rally would be the healthier signal; until that happens, the advance remains vulnerable to a sharp rotation if leadership stumbles.

Rate expectations remain the swing factor. Softer inflation prints have pulled forward the debate about when policy easing begins, and any renewed uptick in yields could quickly cool the multiple expansion that has powered the recent leg higher.

For newcomers, the lesson is straightforward: strong indices can still hide uneven risk. Positioning around confirmed trends, with defined stops, matters more than chasing a headline high that a handful of stocks are carrying.

Seasonally, the second half of the year has often favoured US equities, and the current setup leans on that tailwind. But seasonality is a tendency, not a promise, and the Asia weakness is a live counterexample of how regional shocks can spill into global risk appetite within a single session.

The dollar's drift lower has also helped. A softer greenback supports multinational earnings translated back into dollars and eases financial conditions, giving the index another quiet tailwind beneath the megacap headlines that grab attention.

Practical takeaway: the trend is up, but its foundation is narrow. Traders who respect the leadership while hedging the breadth gap tend to navigate these late-cycle advances better than those who assume the index level equals broad strength.

A final note on risk: the same megacap concentration that drives the index higher also means a stumble in one or two leaders could pull the whole benchmark with it. That is the trade-off of a narrow rally, and it is why measured position sizing matters more than conviction alone.

If the data cooperate, the path of least resistance stays higher into the next print. But the Asia session is the canary: when global risk appetite turns, it often shows up first in the regions most exposed to trade and tech cycles, well before Wall Street feels it.

Putting it together, the US index looks constructive but top-heavy. Traders who want exposure can lean on the trend while keeping one eye on Asian equivalents and Treasury yields, because those are the early-warning gauges that have preceded every rotation in this cycle.

For the session ahead, the base case is a modest grind higher as long as yields cooperate and megacap leadership holds. The risk case is a catch-down if Asian weakness spreads, so the sensible posture is to trade the trend while respecting the narrow base beneath it.

Trading Insight

US indices hold a strong uptrend as cooling inflation and solid earnings lift sentiment, but the Asia sell-off shows risk can rotate fast; track yields and mega-cap leadership.